Building a $20,000/Month Income Engine: The Disciplined Approach to a $1M Portfolio

How to shift from hoping for capital appreciation to mathematically leasing your capital using Cash-Secured Puts, Covered Calls, and the Wheel Strategy.

Building a $20,000/Month Income Engine: The Disciplined Approach to a $1M Portfolio

Most retail investors view the stock market purely as a vehicle for capital appreciation. They buy, they hold, and they pray for the price to go up. But institutional titans look at capital differently. They view capital as an inventory that can be systematically leased out to generate robust cash flow.

If you have a $1,000,000 portfolio, shifting your mindset from "appreciation" to "yield" unlocks a completely new trajectory. Generating a safe, sustainable 1.5% to 2% monthly return translates to $15,000 to $20,000 per month in pure cash flow.

Here is the exact, disciplined architecture required to build that engine using Cash-Secured Puts, Covered Calls, and the Wheel Strategy.

The Asymmetry of Selling Insurance

"In 1993, Berkshire Hathaway sold out-of-the-money put options on 5 million shares of Coca-Cola, collecting $7.5 million in premium. Our logic was simple: we were willing to buy the stock at a lower price, and we got paid a massive premium for making that commitment." — Warren Buffett (1993 Shareholder Strategy)

If legendary value investors generate income by selling options, why does retail look at them as gambling? Because retail buys options. When you use the Wheel Strategy, you switch sides. You become the casino. You collect the premium from the impatient speculators while letting Theta (time decay) do the heavy lifting in your favor.

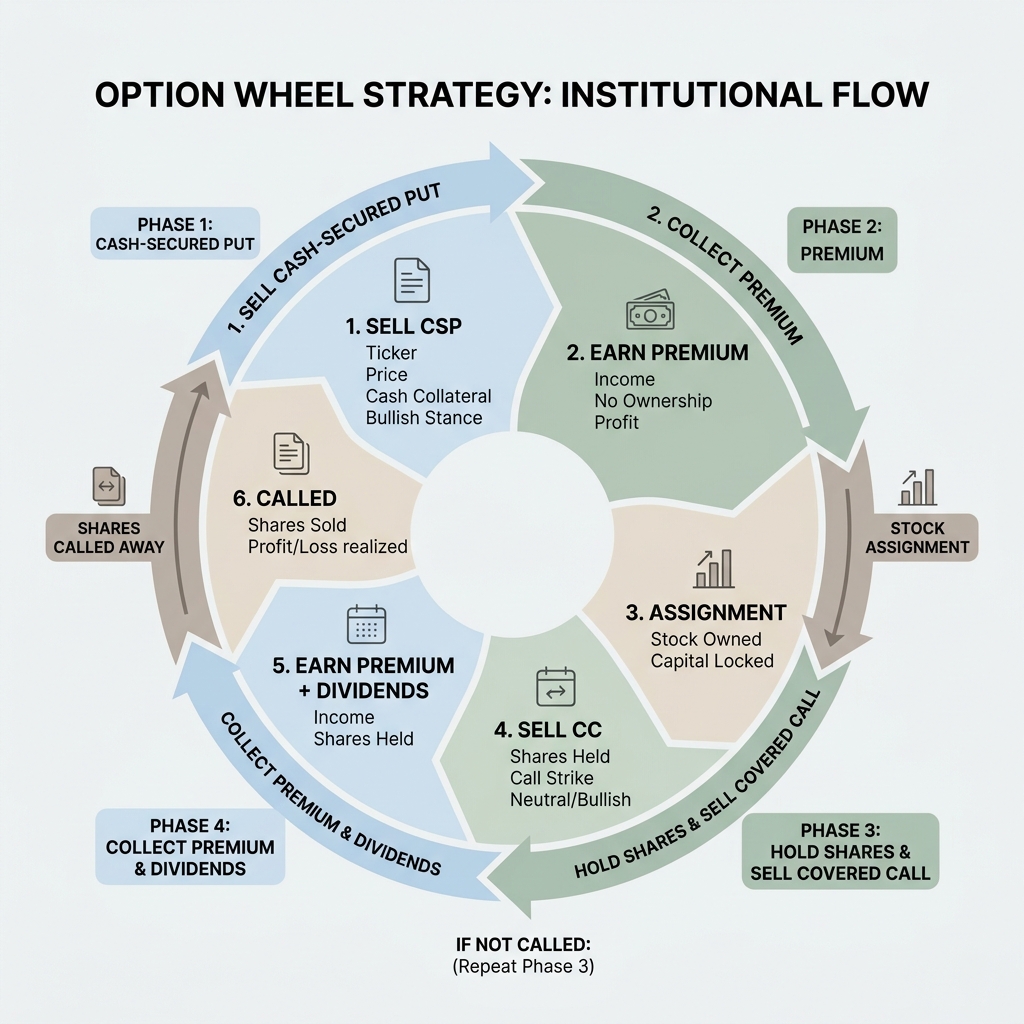

Visualizing The Wheel Strategy Loop

This engine is powered by a fundamentally simple loop: Holding cash to sell puts, acquiring the stock at a discount to sell calls, and eventually having your shares called away to harvest both capital gains AND premium. Let's mechanically drill down into exactly how Phase 1 and Phase 2 work:

Mechanics: The Cash-Secured Put (CSP)

With our $1M portfolio, we maintain a heavy cash buffer. When you sell a CSP, you are essentially placing a limit order to buy a stock you love at a massive discount, and getting paid cash upfront to wait.

The Setup: You configure $10,000 in your account. The Trade: You sell one $95 Put Option against a blue-chip stock for a $200 Premium. The Payout: You collect $200 cash immediately (+2% immediate yield).

At Expiration (The Two Institutional Pathways):

- 🟢 Path A (Stock Stays Above $95): The option expires completely worthless to the buyer. You keep the $200 premium and your $10,000 cash. The routine is safely complete, and you write another put.

- 🔴 Path B (Stock Drops Below $95): You are "assigned" the shares. You are structurally obligated to buy 100 shares at $95. However, since you already collected the $200 premium upfront, your effective, true cost basis is actually only $93 per share. You now own an asset you love at an aggressive discount, and you instantly transition to Phase 2 (Covered Calls).

Mechanics: The Covered Call (CC)

If your CSP gets assigned, you now legitimately own the stock at a discount. Instead of just holding it idly, you immediately transition to Phase 2: Selling Covered Calls against your new inventory.

The Setup: You now own 100 Shares of AAPL (currently trading at $150). The Trade: You sell a single $160 Call Option against those shares for a $200 Premium. The Payout: You collect $200 cash immediately against your existing, idle inventory.

At Expiration (The Two Institutional Pathways):

- 🟢 Path A (Stock Stays Below $160): The option expires worthless to the buyer. You simply keep the $200 premium, and you still own your 100 shares. You sell another Call option the following week to double-dip.

- 🔴 Path B (Stock Surges Above $160): Your portfolio shares must be sold to the buyer for $160. You successfully capture the $1,000 underlying capital appreciation plus the $200 premium you collected on day one. Total Profit is $12 per share.

Building the System: The "Monday Routine"

Discipline is the defining trait of institutional traders. Let's mathematically break down exactly how you execute this on a weekly basis, rather than checking charts multiple times a day.

The Exact Math (5% - 10% OTM Routine):

- Asset Base: You own $400,000 in high-quality tech index ETF shares (e.g., QQQ) trading around $400 per share. That perfectly equates to 1,000 shares (or 10 Option Contracts).

- The Monday Action: On Monday morning, you identify the weekly call option expiring on Friday that is 5% Out-of-the-Money (Strike price: ~$420).

- The Transaction: You sell 10 contracts at a ~0.15 Delta. The premium collected is roughly $1.00 per share.

- The Income Flow:

10 contracts × 100 shares × $1.00 = $1,000 in cash collected immediately.

The Outcomes By Friday:

- QQQ stays under $420: The options expire worthless. You keep your $1,000 cash. You perform the exact same routine next Monday.

- QQQ rockets past $420: Your shares are called away at $420. You keep the $1,000 premium plus you made $20,000 in underlying capital gains.

If you repeat this highly conservative, mathematically defined routine across your $1,000,000 portfolio yielding roughly $2,500 every single week (combining Calls and Puts), you create a robust baseline income of $10,000 per month without ever liquidating principal.

The $1,000,000 Hypothetical Breakdown

Let's look at a highly conservative monthly architecture utilizing a structured tier hierarchy:

🟢 Tier 1: Risk-Free Cash Buffer (30%)

- Strategy: Hold in a 5% Money Market Yield Fund

- Target Delta: N/A (Zero Market Risk)

- Capital Allocated:

$300,000 - Expected Monthly Output:

~$1,250

🔵 Tier 2: Core Equity Holdings (40%)

- Strategy: Sell Weekly Covered Calls on quality, low-IV Equities

- Target Delta: 0.15 - 0.20

- Capital Allocated:

$400,000 - Expected Monthly Output:

~$4,800

🔴 Tier 3: Tactical Cash Reserves (30%)

- Strategy: Sell Cash-Secured Puts into High-IV Market Spikes

- Target Delta: 0.25 - 0.30

- Capital Allocated:

$300,000 - Expected Monthly Output:

~$7,500

🏆 Master Output Summary:

- Total Capital Deployed:

$1,000,000 - Estimated Monthly Cash Flow:

$13,550 - (Achieving a massive ~16% conservative annualized yield)

Note: If you push your Delta up to 0.35 during high implied volatility periods (when premiums swell), that $13.5k figure effortlessly scales past $20,000+ per month.

How OptionsMastery.ai Automates the Math

Executing this routine manually is completely possible, but it requires hours of scrolling through options chains and calculating net yields. This is exactly what we built OptionsMastery.ai to solve.

1. Smart Money Convergence

Selling a Put is safest when you know institutional size is supporting the stock. Our Smart Money dashboard aggregates real-time 13F and prime broker data. If Citadel and Jane Street are accumulating massive $250M+ blocks of a specific asset on a dip, our engine flags it. You sell your Puts exactly where the big boys place their floor.

2. The Athena AI Copilot

You don't need to manually calculate the "Monday Routine." Just ask Athena AI: "I have 1,000 shares of QQQ. Find me the optimal Covered Call expiring this Friday that yields at least $1,000 in premium but stays under 0.20 Delta." Athena will instantly calculate the Greeks, filter the entire chain, and present the precise contract.

3. Systematic Intelligence

We track your capital allocation automatically. The dashboard dynamics update to ensure you never over-leverage a single sector, keeping your $1M engine perfectly balanced.

Stop guessing. Start generating yield.

Ready to put this into practice?

Join OptionsMastery.ai today and let Athena instantly find the optimal strategies for your portfolio.

Start Free Trial